Breaking the mental barriers that keep 1.4 billion people away from wealth creation

A Scene We All Know Too Well

Picture this: You’re at a family dinner, and the topic of money comes up. You mention that you’ve started investing in mutual funds or the stock market. Before you finish, an uncle leans forward and says, “Beta, share market is gambling. Fixed Deposit is safe. At least your money stays in front of your eyes.”

Heads nod in agreement, the topic shifts, and just like that, the market is declared dangerous. If this sounds familiar, you’re not alone. In India, our relationship with money is deeply emotional. For decades, the Indian dream has been less about aggressive wealth creation and more about safety. We gravitate towards what feels tangible:

– Gold stored in lockers

– Houses made of brick and cement

– Bank passbooks with stamped entries

The Great Indian Paradox: Growth Without Inclusion and Awareness Without Action

India’s capital markets are witnessing unprecedented growth. Demat accounts, SIP registrations, and retail participation are all at all-time highs. Millions of new investors have entered the ecosystem over the last few years, driven by digital platforms, fintech innovation, and rising market awareness.

Yet, this growth masks a deeper structural problem.

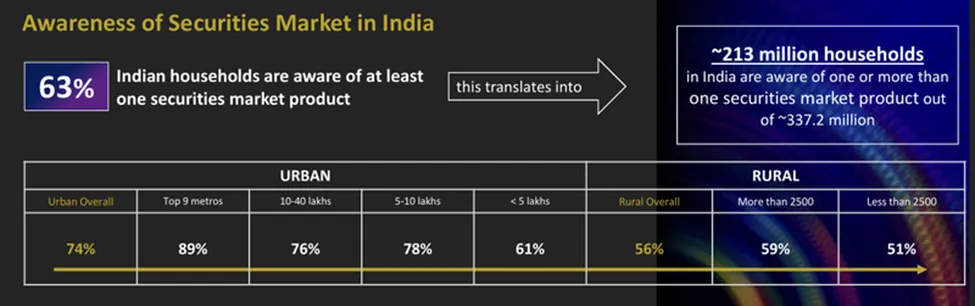

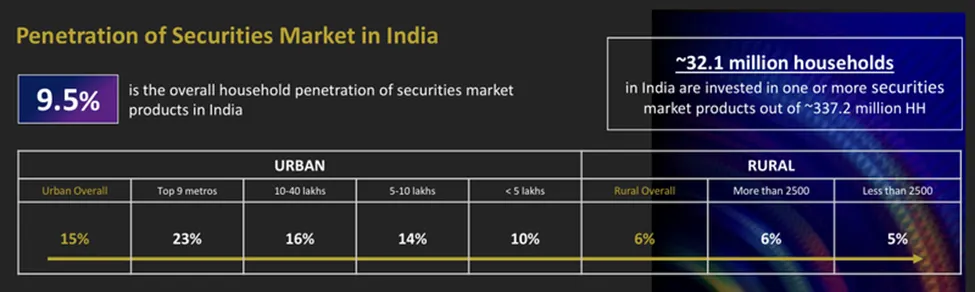

According to the SEBI Investor Survey 2025, while 63% of Indian households are aware of securities market products, only 9.5% actually invest. Participation remains geographically and socially skewed. Around 15% of urban households participate, while rural participation is just 6%.

Out of nearly 140 crore Indians, only about 5–6 crore actively participate in equity markets. This means that despite visible growth metrics, market penetration and financial inclusion remain limited.

As a result, an estimated $10 trillion of household savings remains locked in physical assets or low-yield instruments instead of flowing into productive financial markets. Awareness exists, but the trust bridge is broken — held back by fear, complexity, and lack of confidence.

Understanding the Roots of Fear

1. Historical Memory and Market Trauma

The fear of the stock market in India is not irrational; it is rooted in history. Many households lived through the Harshad Mehta securities scam of 1992 and the Global Financial Crisis of 2008. In 1992, the Sensex fell from nearly 4,500 to 2,500, wiping out the life savings of thousands of middle-class families. For those who experienced it, the stock market did not represent opportunity; it represented loss.

This collective trauma has shaped household beliefs. When one generation loses money to what they perceive as “paper wealth,” the next generation is taught to trust only what is tangible. The phrase “share market is gambling” reflects a learned survival response.

2. Conditioning Towards Safety Over Growth

Indian households have historically prioritized capital protection over capital growth. Culturally, we are taught that fixed deposits are safe, gold is traditional and reliable, real estate is tangible and controllable, and equity markets are risky and speculative.

This conditioning made sense when markets were less accessible and information was scarce. However, times have changed. While saving is essential, if the return on investment is lower than the rate of inflation, the value of savings may decrease.

3. Entering the Market at the Worst Possible Time

Another pattern observed among Indian investors is poor timing. People typically enter the market when markets are making headlines, indices are near all-time highs, friends share success stories, or social media amplifies short-term gains.

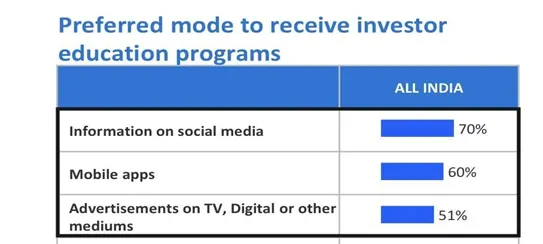

The Investor Survey 2025 conducted by SEBI highlights that the majority of the Indian population relies on social media, mobile apps, and TV/digital advertisements for financial education. After a digital media hype, when markets inevitably correct, fear takes over. Investments are exited prematurely, losses are realized, and the blame is placed entirely on the market.

In reality, the issue is rarely the market itself; it is entering without preparation, strategy, or understanding.

4. Limited Financial Education and Behavioral Biases

The study of behavioral finance in India is still in its early stages. Individual investors are influenced by cognitive and emotional vulnerabilities, including loss aversion, herd behavior, and overreaction to short-term movements. Most Indians are never formally taught how compounding works, why volatility is normal, the difference between investing and trading, or how long-term wealth is created.

When understanding is missing, fear naturally fills the gap.

5. Risk Tolerance, Demographics, and Lack of Guidance

Investment decisions are shaped by risk capacity, demographics, and access to financial advice.

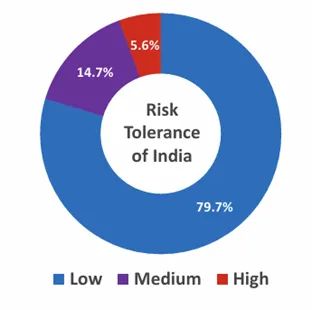

The SEBI Investor Survey 2025 reveals that 79.7% of Indian households exhibit low risk tolerance, with a priority on protecting capital rather than maximizing returns. Among non-investors, the fear of losing money due to market volatility remains the strongest reason for avoiding securities markets.

This low tolerance is further reinforced by complex financial products with hidden charges, promises of high returns with low risk, and one-size-fits-all solutions. Most households have never received goal-based planning, clear risk explanations, or transparent discussions around trade-offs. In the absence of clarity, avoidance feels safer, which is why the survey identifies three core barriers to investing:

– Lack of clear, accessible information

– Difficulty in accessing and navigating investment platforms

– Low trust in intermediaries and market systems

Therefore, non-investors are more likely to participate when the aforementioned barriers are removed i.e. investment process is simplified, knowledge levels improve in practical ways, and trust is built through transparency and accountability. The shift from saving to investing does not come from higher return promises, but from clarity, confidence, and credible guidance.

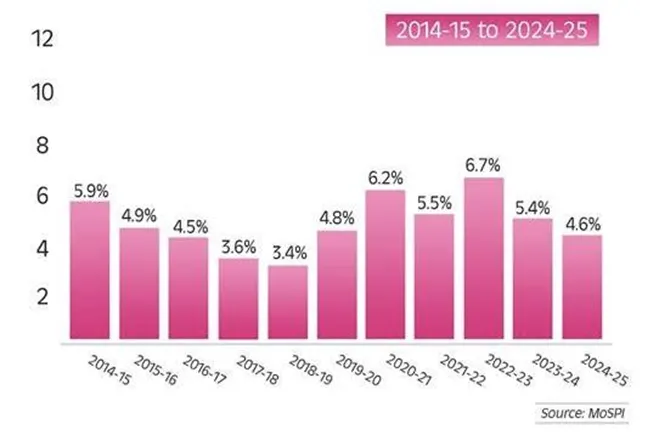

The Silent Cost of Playing It Safe: Inflation

Here’s the uncomfortable truth: inflation quietly erodes wealth without drawing attention to itself. In India, retail inflation as measured by the Consumer Price Index (CPI) has largely hovered between 5% and 7% over long periods. For essential household expenses such as food, fuel, healthcare, education, and housing, inflation often runs even higher.

When savings earn returns close to these levels, the perception of safety can be misleading. After accounting for inflation — and taxes in many cases — the real purchasing power of money declines steadily. This erosion is not sudden or dramatic; it is silent, persistent, and compounding.

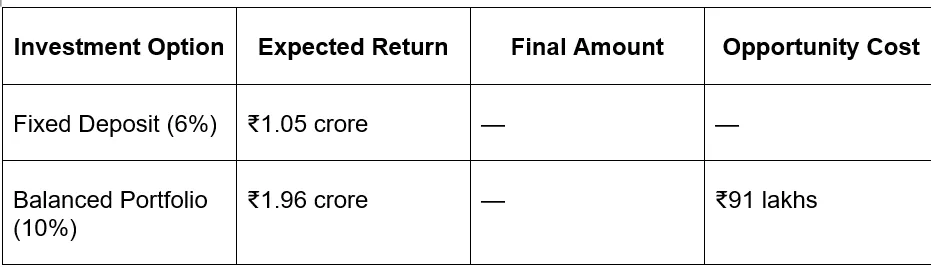

To understand the real impact, consider this scenario:

Scenario: ₹15,000 Invested Monthly for 25 Years

That ₹91 lakh difference is not the result of reckless risk-taking; it is the cost of avoiding growth. Even more striking, ₹1 lakh kept in a savings account today will have the purchasing power of approximately ₹61,000 after 10 years due to inflation.

What feels safe is often the biggest long-term risk.

Moving From Fear to Structure: What Actually Works

Fear does not disappear through motivation or market tips; it reduces when investing is approached with structure, clarity, and purpose.

1. Redefining Risk

Market volatility is not the biggest risk investors face. The real risks are failing to beat inflation, falling short of life goals such as retirement or education, and running out of money later in life. Avoiding equity may feel comfortable, but it carries a hidden and compounding cost.

2. Replacing Guesswork With SIP Discipline

One of the most common mistakes is trying to time the market — buying late and exiting early. A more effective approach is Systematic Investment Plans (SIPs):

– Invest a fixed amount every month

– Automatically buy more units when markets fall and fewer when they rise

– Reduce emotional decision-making through rupee cost averaging

– Begin with amounts as small as ₹500 per month

This approach turns volatility from a threat into an advantage.

3. Separating Survival From Growth

Fear often stems from the worry of needing invested money in the short term. The solution is simple:

– Maintain an emergency fund covering six months of expenses in liquid instruments

– Invest only surplus money meant for long-term goals

Once short-term needs are secured, long-term investments feel far less stressful.

4. Diversifying for Balance, Not Excitement

A portfolio should be balanced, not extreme. Just as a proper meal needs variety, so does investing. A diversified approach could include:

● large-cap funds for stability

● mid-cap funds for growth

● small-cap funds for higher long-term potential

● gold or debt funds to cushion volatility

● international funds for diversification, offering exposure to global businesses and US dollar–denominated assets that may help hedge against long-term rupee depreciation, while being mindful of taxation, currency volatility, expense structures, and additional costs — especially when investing directly overseas

5. Investing With Purpose

Fear thrives in uncertainty. Purpose creates discipline. When investments are linked to specific goals such as retirement security, children’s education, buying a home, or building long-term wealth, short-term fluctuations matter less.

6. Letting Time Do the Heavy Lifting

Markets will always rise and fall; that is their nature. History consistently shows that long-term investors are rewarded, patient capital outperforms reactive capital, and time in the market matters more than timing the market.

7. Seeking Guidance, Not Just Products

Products don’t manage fear; plans do. Effective financial guidance focuses on individual goals and timelines, genuine risk tolerance, long-term wealth creation, and periodic review and rebalancing.

The Final Takeaway

The biggest risk isn’t market volatility; it’s not starting at all. Your “safe” fixed deposits are slowly losing value to inflation. Your gold isn’t generating income, and your real estate is illiquid when you need cash.

It’s time to stop being just a “saver” and start being a “wealth creator.” Remember: you don’t need to be rich to invest; you invest to become rich.

Start small, start simple, but start today. Your future self — and that uncle at the next family dinner — will thank you.

References

- Securities and Exchange Board of India (SEBI). (2025, September 30). SEBI Investor Survey 2025. Government of India.

- Ministry of Finance, Government of India. (2025, April 16). India’s Retail Inflation Hits Six-Year Low: Retail Inflation Drops to 4.6% in FY 2024–25. Press Information Bureau (PIB).