The Estate Planning Checklist: The Definitive Guide to Wealth Succession

Estate planning is not just paperwork for the wealthy or the old. It is the one financial

conversation most people keep postponing until it is too late to have it well.

You invest carefully. You insure what matters. You plan for retirement. And yet, the one

document that decides what happens to everything you have built often does not exist. Or if

it does, it was written once, filed away, and never looked at again.

Estate planning is the process of deciding, in advance, who gets what, who makes decisions

on your behalf, and how your wishes are carried out without confusion or conflict. It is not

morbid. It is one of the most caring things you can do for the people you leave behind.

What Is an Estate?

Most people think “estate” means a mansion. It does not. Your estate is everything you own:

● House, land, or property

● Bank accounts and fixed deposits

● Investments: mutual funds, stocks, bonds

● Insurance policies

● Gold and valuables

● Business interests

● Digital assets: crypto, trading accounts, domain names

If you own anything, you have an estate. And it needs a plan.

Who Actually Needs Estate Planning?

Short answer: almost everyone. If you have a spouse, children, dependent parents, property,

savings above ₹5 lakhs, or run a business, you need it. You especially need it if you have

minor children (guardian appointment is critical), a special needs dependent, a blended

family, or significant digital assets.

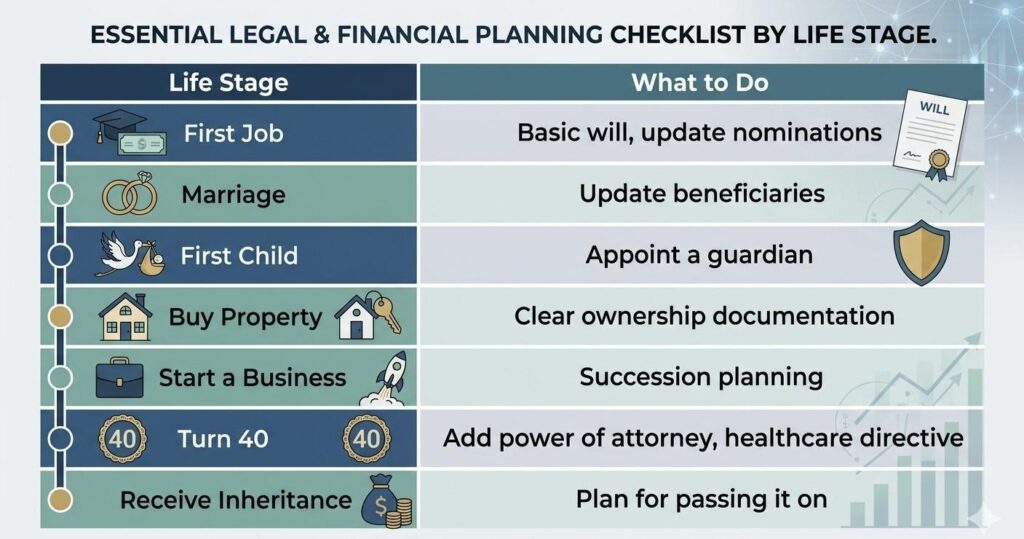

The right time to start retirement and estate planning is not “someday.” It is now. Here is a

simple guide:

And then update your plan after every major life event such as marriage, divorce, the birth of

a child, the death of a nominee, or any significant change in assets. A plan reviewed every

three to five years is the one that actually works when needed.

The Three Primary Tools

Tool 1 —> The Will

A Will is a legal document that specifies how your assets should be distributed after your

death, names an executor to carry out your instructions, and critically appoints a guardian for

your minor children. No other document does this.

A will comes into effect only after you pass away. When you do, it must go through probate

which is a court-supervised process where the will is validated and the distribution is

overseen. Without a will, your estate is distributed according to the personal law applicable

to you: the Hindu Succession Act, the Indian Succession Act, or Muslim Personal Law.

These follow a fixed formula that may have nothing to do with what you actually wanted.

How to make a Will:

List every asset and liability including bank accounts, investments, property,

insurance, vehicles, jewellery, business interests, outstanding loans.

Name beneficiaries specifically. “My daughter Priya”, not just “my children.”

Ambiguity is the most common source of will disputes.

Appoint a trustworthy executor (ideally someone younger than you).

Name a guardian for any minor children. Without this, a court decides who raises

them.

Draft the document clearly, stating it is your last will and testament, dated, with

unambiguous intentions.

Sign in front of two witnesses who are not beneficiaries, both present simultaneously.

Register it at the Sub-Registrar’s office (optional but strongly advisable) as it makes

the will significantly harder to challenge later.

Store it safely and tell your executor exactly where it is. A will nobody can find is as

good as no will at all.

Tool 2 —>The Trust

A Trust is a legal arrangement where you transfer ownership of assets to a trustee, who

holds and manages them for the benefit of your chosen beneficiaries according to rules you

set out in a trust deed.

Unlike a will, a trust can be active during your lifetime. A revocable living trust, for

example, lets you remain in control of your assets while alive, and automatically transfers

them to beneficiaries upon death bypassing probate entirely.

Every trust involves three parties:

● Settlor: you, the one who creates and funds the trust

● Trustee: the person or institution (family member, trust lawyer, or bank trust

department) who manages the assets with a fiduciary duty to act in beneficiaries’

interests

● Beneficiaries: those who receive the benefit, as per your conditions

Types of trusts:

● Revocable Living Trust: You stay in control, can modify or dissolve it anytime.

Assets transfer to beneficiaries on death without probate. Best for flexibility and

seamless succession.

● Irrevocable Trust: Cannot be changed once created. Assets are legally no longer

yours. Used for tax planning, creditor protection, and long-term charitable giving.

● Testamentary Trust: Created by a will, comes into effect only after death. Useful for

holding assets for a minor until they reach a specified age. Subject to probate since it

originates from a will.

● Special Needs Trust: For a beneficiary with a disability. Provides financial support

without disqualifying them from government welfare schemes.

● Charitable Trust: Benefits a charitable purpose. Registered trusts under the Income

Tax Act can receive tax benefits. It’s often used for lasting philanthropic legacies.

● Family / HUF Trust: Structured around a Hindu Undivided Family to hold and

manage wealth across generations, preventing fragmentation through partition

disputes.

How to set up a trust:

Define your purpose — protecting a minor, managing a dependent’s future, avoiding

probate, or philanthropy?

Identify all three parties: settlor, trustee, and beneficiaries.

Draft the trust deed with a trust lawyer.

Execute the deed signed by the settlor and trustee before witnesses. If immovable

property is involved, registration with the Sub-Registrar is mandatory.

Transfer assets into the trust — retitling bank accounts, conveying property,

transferring investments.

Appoint a successor trustee.

Review periodically when your financial situation, family structure, or applicable law change.

Note:

● A trust does not replace a will. Most estate plans use both: a will for assets never

transferred into the trust, and the trust for everything that was.

● Setting up a trust involves real expenses. Drafting the trust deed with a trust lawyer,

registering it, and transferring assets all carry fees. Property transfers into a trust, for

instance, typically attract stamp duty of 2–3% of the market value. These costs vary

by state and asset type and should be factored into your planning before deciding

whether a trust is the right tool for you.

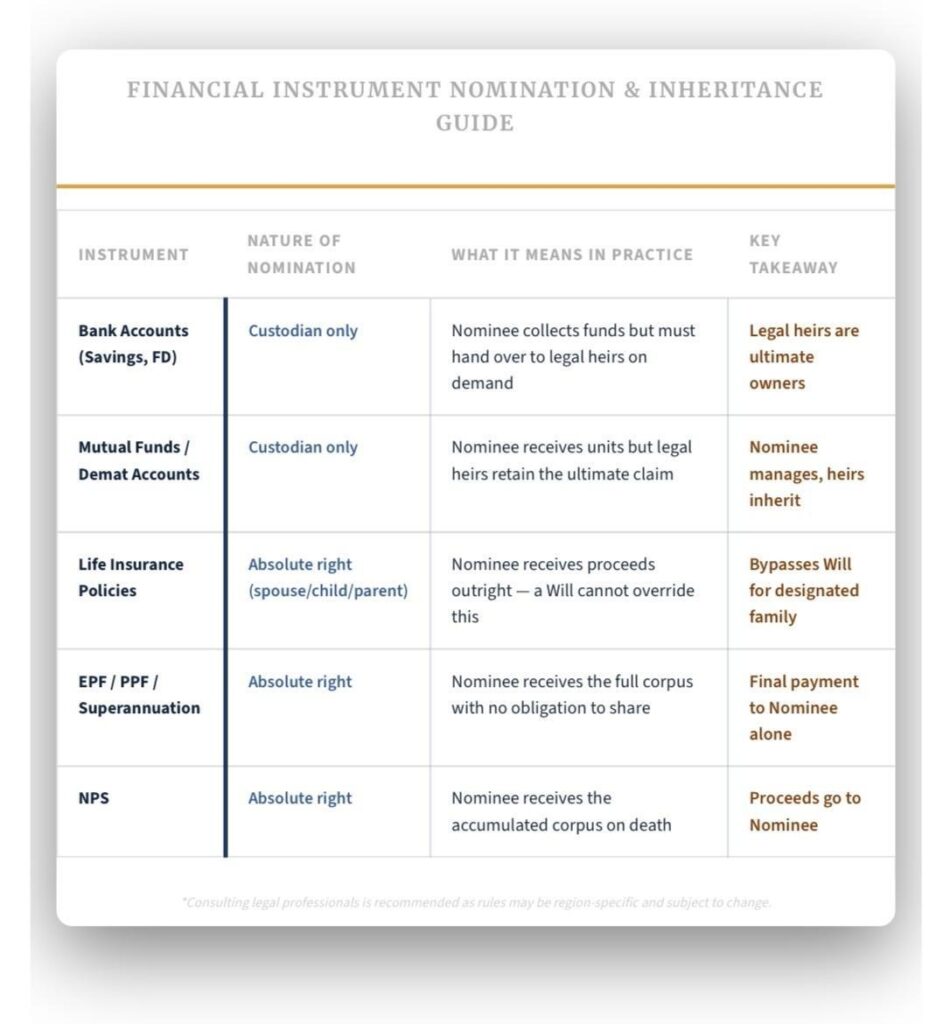

Tool 3 —> Nomination

Nomination is a facility offered by financial institutions that allows you to designate a person

to receive your assets such as bank balances, insurance proceeds, mutual funds, and

provident fund in the event of your death.

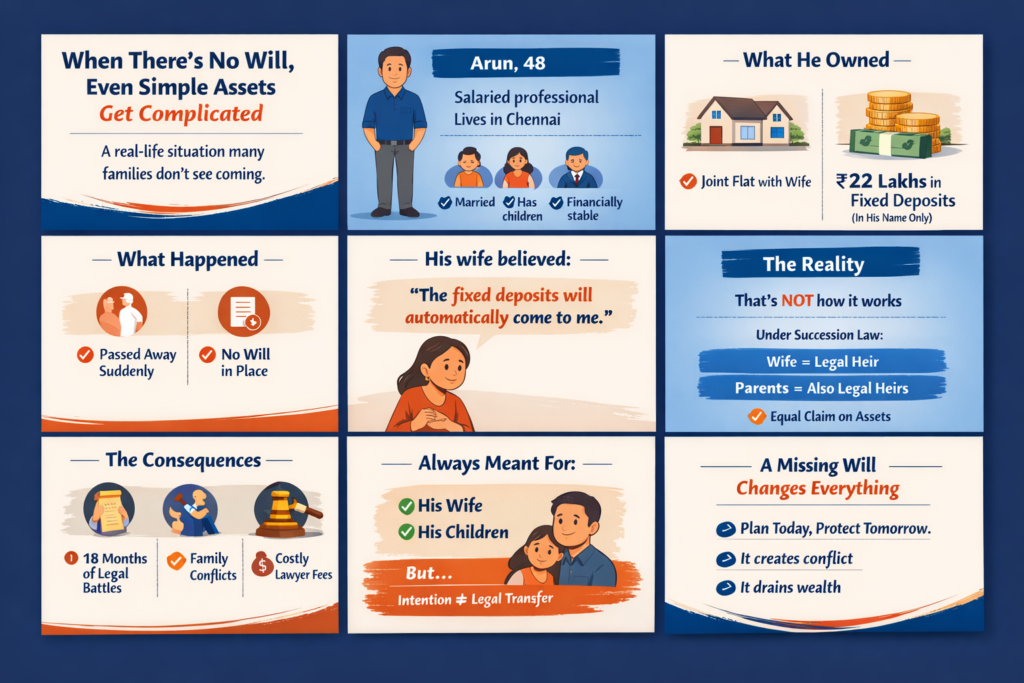

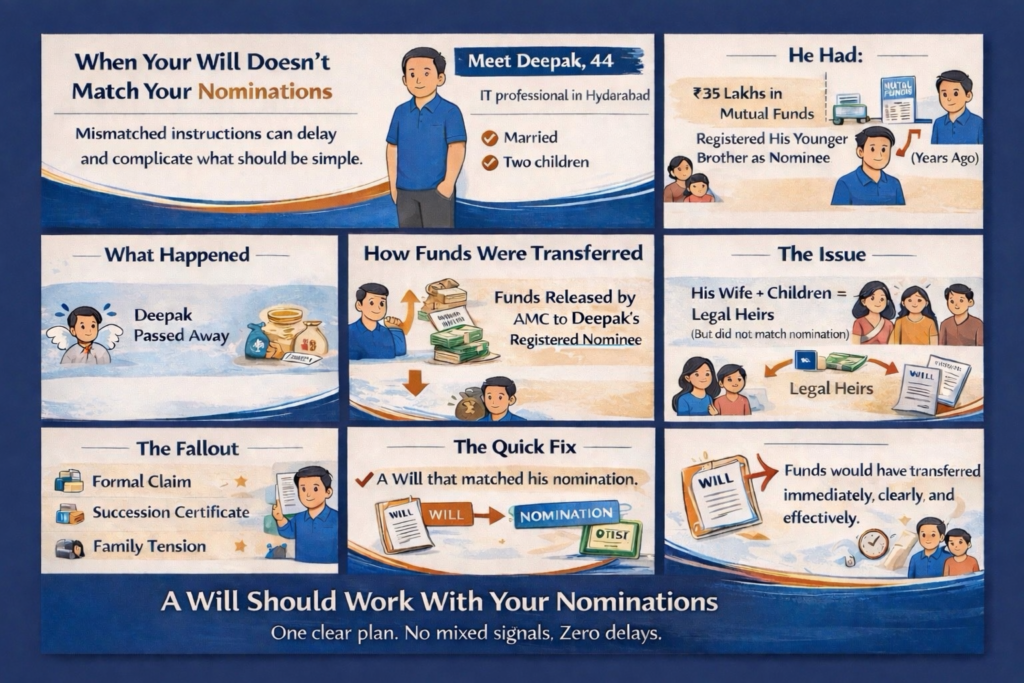

It is the most widely used estate planning tool in India, and the most misunderstood.

The critical distinction: a nominee is not automatically an heir. Think of them as the

“delivery person” for your assets, not the final recipient. For most financial instruments, a

nominee is a custodian who receives the money and holds it until the legal heirs claim it

based on succession law or a will.

Where nomination applies:

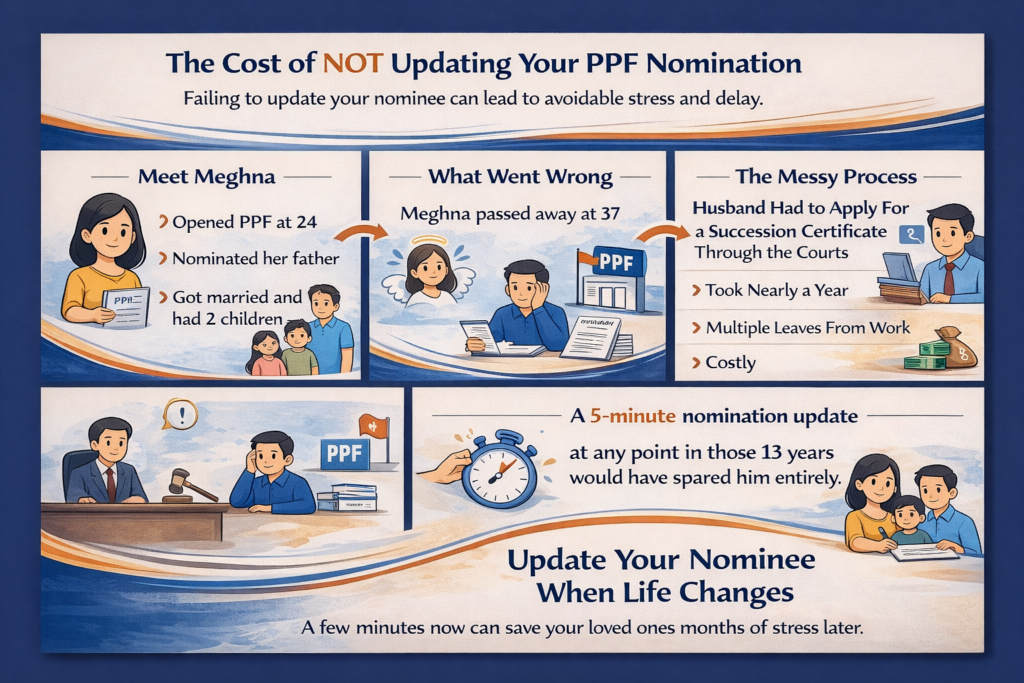

Three mistakes most people make:

Not nominating anyone: the bank or AMC requires a legal succession certificate,

which can take 6 to 24 months.

Nominating a minor: the payout is frozen until the child turns 18 unless a guardian

is also appointed.

Not updating after life events: if your nominee passes before you, the nomination

becomes void.

To update nominations: list every account you hold, check current nominees, submit a

change form (online or at a branch), nominate multiple people where instruments allow, and

align nominations with your will so both tell the same story.

Updating a nomination takes fifteen minutes. Not updating it can take your family fifteen

months of paperwork and legal hearings.

The Five Missing Pieces

Most people stop at writing a will or updating a nomination. But estate planning is more than

deciding who gets your assets. These are the elements most often missed and whose

absence creates real, serious problems.

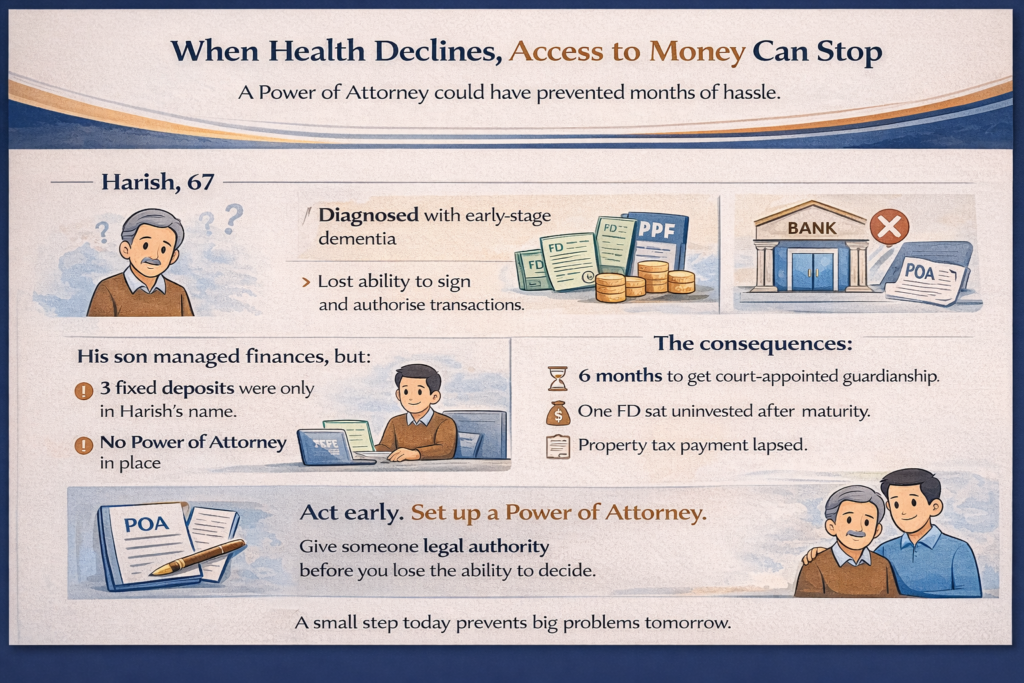

Power of Attorney (POA)

A will only kicks in after death. What if you are alive but incapacitated after a stroke,

accident, or cognitive decline?

A Power of Attorney appoints someone to manage your finances and make decisions on

your behalf while you are still alive. A general POA covers broad decisions; a specific POA is

limited to a defined purpose.

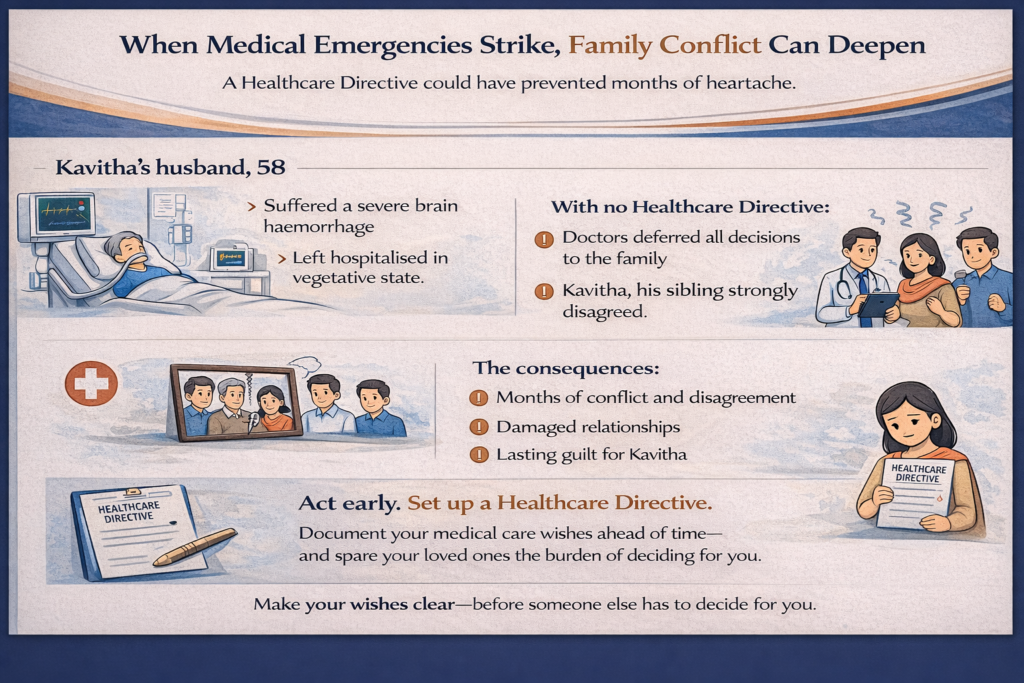

Healthcare Directive (Living Will)

What medical treatment do you want or refuse if you cannot speak for yourself? Which

treatments? Life support decisions? Organ donation?

A healthcare directive records your medical wishes so doctors and family are not left

guessing. It is legally valid in India since the Supreme Court’s landmark 2018 ruling.

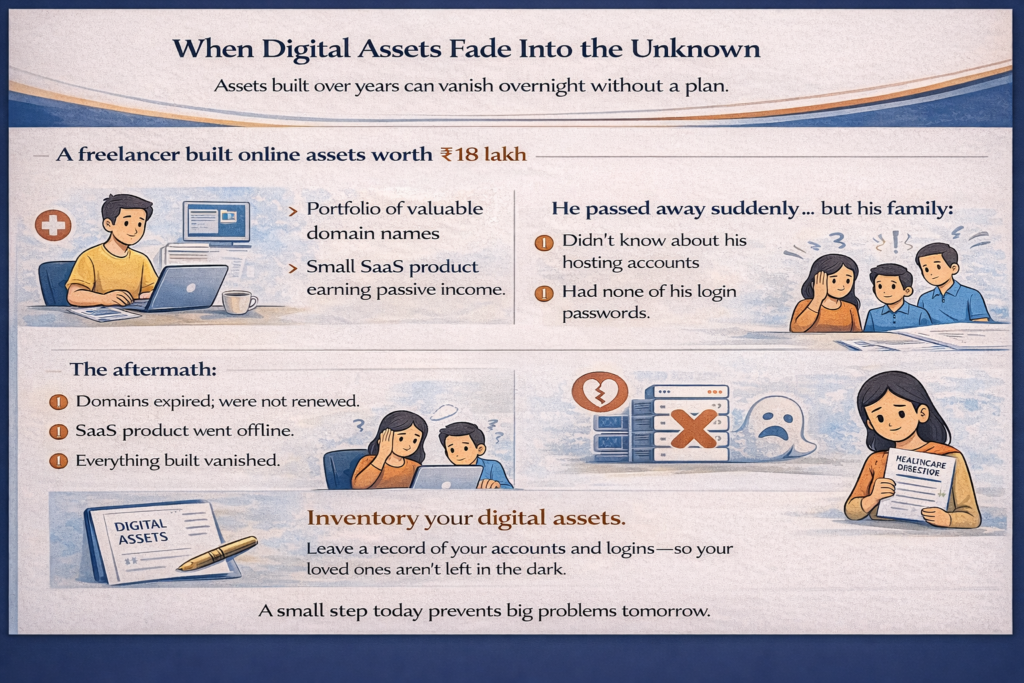

Digital Assets Inventory

Email accounts, cryptocurrency wallets, trading accounts, cloud storage, social media

profiles, domain names, UPI accounts, digital businesses — most people have significant

value locked in digital assets with no access instructions left behind.

If you do not document them and share access securely, they are effectively gone forever.

A secure password document stored alongside your will is a simple but powerful starting

point.

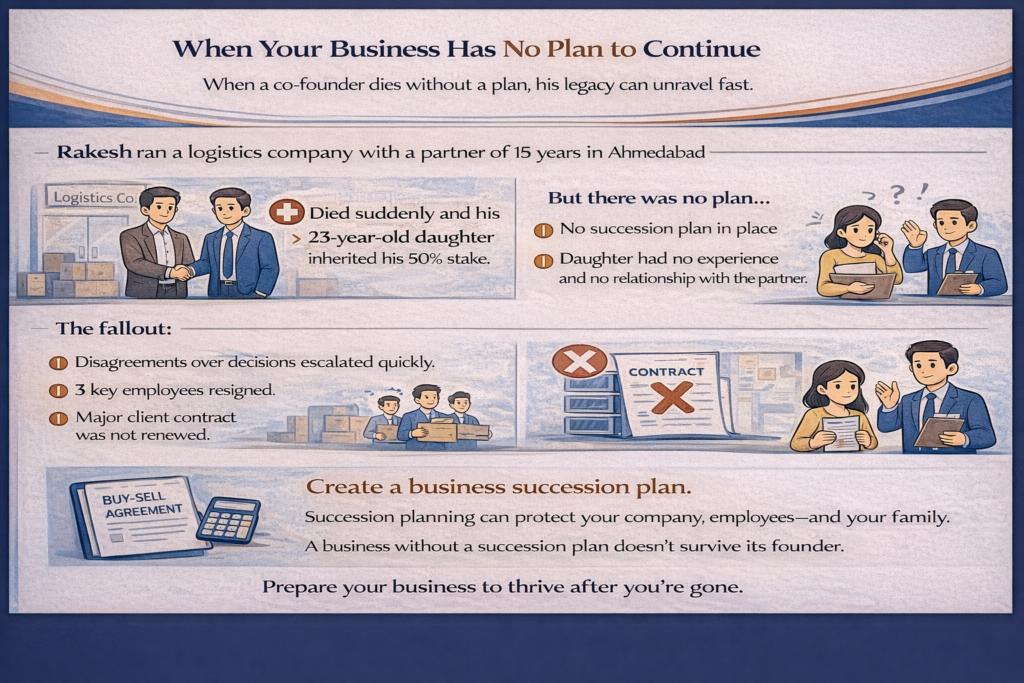

Business Succession Plan

A will says who gets your shares not who runs the business, or how disputes are handled.

Without a succession plan, a profitable business can collapse within months of an owner’s

death.

A buy-sell agreement or formal succession plan prevents this entirely.

The Master Information Vault

Your family should never have to play detective after you are gone. One document shared

with your executor should include: all bank accounts and FDs, insurance policies, investment

accounts, property document locations, locker keys and contents, and the location of your

will.

This is not glamorous estate planning. But it is often what saves families the most time and

anguish.

Putting It All Together

A will tells your loved ones what you owned. A trust decides how it is managed. A

nomination ensures quick access to specific assets. A power of attorney protects you while

you are still alive.

A healthcare directive speaks for you when you cannot. A digital inventory

and a business succession plan close the gaps everyone else leaves open.

The goal is not to predict every outcome. It is to remove the burden of uncertainty from the

people who will already be grieving. When your wishes are clearly documented, your family

does not have to guess. They do not have to fight. They can simply grieve and then begin to

move forward.

If you have not started, start with a will. If you have a will, check your nominations. If

your nominations are updated, look at the missing pieces. There is always a next step,

and every step matters.

Estate planning is not a one-time event. It is a document that should grow alongside your

life, your family, and your wealth.

Your legacy is not just what you leave behind. It is how clearly you left instructions for it.